Payment Details

Payment states & events

Use the below diagram for guidance of how Payments (credit-transfers as well as direct-debits) transitions through various states. While we would consider changing the possible state transitions a non-backwards compatible change of the API, it is not recommended to have clients strictly locked down as the diagram shows.

| State | Description |

|---|---|

CREATED | The payment has been created and is pending approval. |

REJECTED | The payment has been rejected by the customer. |

APPROVED | The payment has been approved by the customer. |

PENDING_SUBMISSION | Atlar is submitting the payment to the bank. It cannot be edited at this point. |

SENT | The payment has been sent to the bank. |

PENDING_AT_BANK | The payment is stuck in a pending state at the bank. It can for instance be related to insufficient funds or if bank-side signature has been configured. |

ACCEPTED | The payment has been received and accepted by the bank. |

EXECUTED | The payment has been executed by the bank. |

FAILED | The payment has failed. |

RECONCILED | The payment has been reconciled to a transaction on your account statement. |

RETURNED | The payment has been returned by the bank. |

Direct-Debit Mandate states & events

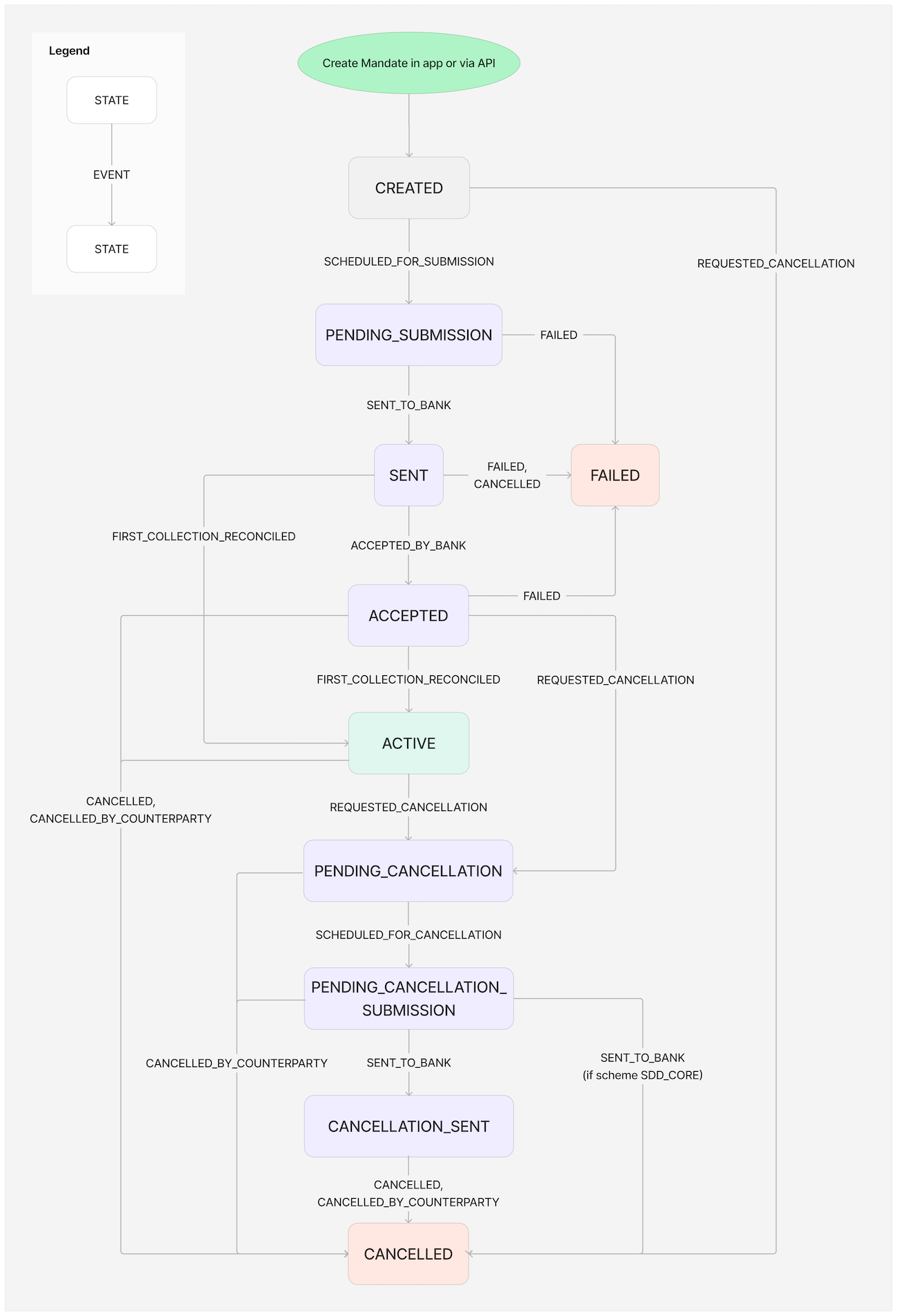

Use the below diagram for guidance of how Mandates transitions through various states. While we would consider changing the possible state transitions a non-backwards compatible change of the API, it is not recommended to have clients strictly locked down as the diagram shows.

| State | Description |

|---|---|

CREATED | The mandate is created (with active=false). How this mandate is sent to the bank will depend on the scheme. E.g. AUTOGIRO mandates are sent directly while SDD ones are sent along-side first payment. |

PENDING_SUBMISSION | Atlar is submitting the mandate to the bank. The mandate cannot be edited after this point. |

SENT | The mandate has been sent to the bank. |

ACCEPTED | The mandate has been received and accepted by the bank. |

ACTIVE | The mandate has been proven working with first reconciled collection, or was created with active=true flag. |

FAILED | The mandate failed to register. This can either be a bank- or Atlar-side error. |

CANCELLED | The mandate has been cancelled, either by you or the counterparty. |

Payment return reason codes

When a credit transfer or direct debit fails, the payment status is updated. The new status will generally be set to either FAILED or RETURNED. To help understand why the payment fails, we forward the payment reason codes from the bank. These codes differ across schemes. For Autogiro, please refer to Autogiro reason codes; for other schemes, refer to ISO.

ISO Originator errors - Credit Transfers & Direct Debits

| Reason Code | Description | Additional Info | Suggested Action |

|---|---|---|---|

| AC03 | Invalid Creditor Account Number | Originator selected or entered the wrong IBAN of the beneficiary. | Update the counterparty to reflect the correct IBAN. |

| BE04 | Missing Creditor Address | Either the Originator PSP or the Beneficiary PSP in the transaction is based in a non-EEA SEPA. country | Originator PSP to ask the Originator to provide the address of the Beneficiary. |

| BE05 | Unrecognised Initiating Party | Creditor: Technical error or omission to report a CI (Creditor Identifier) amendment. | Correct the Creditor Identifier. |

| CNOR | Creditor Bank Is Not Registered | • Creditor PSP is not/ no longer registered as an SDD scheme participant under this BIC at the CSM | Contact the Creditor PSP. |

| MD01 | No Mandate | • Debtor PSP has canceled the mandate under the rule of the 36 months inactivity period; • Debtor PSP was unable to obtain B2B mandate; • Refund for an unauthorised transaction (until 13 months after debit date) (For SDD Core collections only). | • Look into the details of the SDD collection; • Contact the Debtor in case of Refund. |

| MD02 | Missing Mandatory Mandate Information in Mandate | • The way to amend the mandate is not in compliance with the SDD rulebook; • The amended information is not correct. | Make sure that you collect & present all required mandate details during customer onboarding. |

| RC04 | Invalid or Missing BIC | The originator has not included/inserted a correct BIC for a transaction that requires a BIC, such as an international payment or a non-EEA SEPA payment. | In case the BIC is missing, add the BIC for the desired counterparty. In case the BIC is invalid, double-check the entered BIC. |

| RR01 | Missing Debtor Account Or Identification | • Missing details about the Debtor account or identification. • Note: This code cannot be used in certain SEPA countries for reasons of data protection. MS03 could be used as an alternative. | • Contact the Debtor for the correct BIC of a non-EEA SDD Collection. • Ask Creditor PSP to allocate the correct and complete BIC of the Debtor PSP in the inter-PSP message. |

| RR02 | Missing Debtor Name Or Address | • Missing Originator name (address is an optional field for EEA SCT transactions); • Missing address of the Originator for non-EEA SCT transactions. • Note: This code can't be used in certain SEPA countries for data protection reasons. MS03 could be used as an alternative. | Originator Bank to fix the transaction by completing the Originator's name and/or address information. |

| RR03 | Missing Creditor Name Or Address | • Missing Creditor Name (address is an optional field for EEA SDD Collections). For collections in non-EEA countries, including your address is recommended. • Note: This code cannot be used in certain SEPA countries for reasons of data protection. MS03 could be used as an alternative. | • Fix the SDD collection in order to complete the Creditor name; • Contact the Creditor PSP. |

| RR04 | Regulatory Reason | Note: This code cannot be used in certain SEPA countries for reasons of data protection. MS03 could be used as an alternative. | Contact the Creditor PSP. |

ISO Debtor errors, Originator to Contact the Counterparty – Credit Transfers & Direct Debits

| Reason Code | Description | Additional Info | Suggested Action |

|---|---|---|---|

| AC01 | Incorrect Account Number | • Debtor gave incorrect data; • Originator used incorrect IBAN data from its customers' database; • Originator had a technical problem during the processing of collection issuance. | • Contact the Counterparty in order to get the correct IBAN. • For SDD – In case of mandate amendment: check the data provided by the Debtor. |

| AC04 | Closed Account Number | • Counterparty closed their account since the last time the account. • Note: This code cannot be used in certain SEPA countries for data protection reasons. MS03 could be used as an alternative | Contact the Counterparty for new account information or agree on an alternative payment. method. |

| AC06 | Blocked Account | • Account blocked for any financial transaction; • PSP blocked the account or the SDD collection due to a Court Order; • PSP has blocked the account (e.g., suspicion of misuse. | Contact the Counterparty for an alternative account/solution to pay. |

| AC13 | Invalid Debtor Account Type | • Debtor (consumer) was not aware that the signing of a B2B mandate is restricted to non-consumers; • Payment account type does not allow/ support the debiting of SDD B2B collections; • Debtor gave information of a wrong payment account. | • Contact the Debtor for clarification and to agree on another means of payment; • Sign an SDD Core mandate with Debtor instead. |

| AG01 | Transaction Forbidden | • Counterparty gave information of an account which SCT/SDD collections cannot be sent to/booked from (e.g. a savings account). • Note: AG01 cannot be used in the situation of an SDD B2B collection presented to a debtor account that is a consumer account. The code AC13 needs to be used. | Contact the Counterparty in order to agree on another payment account to be used or another payment instrument. |

| AM04 | Insufficient Funds | • Debtor: Insufficient funds on his account; • Creditor: Lack of or late pre-notification announcing the upcoming SDD collection (date and amount). • Note: This code cannot be used in certain SEPA countries for data protection reasons. In this case, MS03 can be used as an alternative. | Contact the counterparty – Ensure that the Debtor provides funds to his account. |

| DNOR | Debtor Bank Is Not Registered | • Debtor PSP is not/ no longer registered as an SDD scheme participant under this BIC at the CSM. | • Ask the Creditor PSP for checking the reachability of the Debtor PSP. • Contact Debtor to agree on another means of payment. |

| MD01 | No mandate | • Debtor PSP has canceled the mandate under the rule of the 36 months inactivity period; • Debtor PSP was unable to obtain B2B mandate; • Debtor has canceled their mandate; • Creditor: 1. Did not use a unique mandate reference (UMR) 2. Provided an SDD collection with a UMR which was not consistent with the mandate information | • Analyse the characteristics of the SDD collection to make sure that the mandate reference is unique & corresponds to the signed mandate. • Contact the Debtor in case of Refund. |

| MD06 | Refund Request by End Customer | • Unconditional Refund of Collection (SDD Core – until 8 weeks after debit date); • Discrepancy between the amount announced in the pre-notification and the amount of the SDD Core collection; • Unconditional Refund right under the Payment Services Directive (PSD). | Contact the Debtor. |

| MD07 | End Customer Deceased | • Deceased. • Note: This code cannot be used in certain SEPA countries for data protection reasons. In this case, MS03 can be used as an alternative. | Close the agreement with the deceased Counterparty. |

| MS02 | Not Specified Reason Customer Generated | • Debtor receiving the prenotification decided to refuse the collection. | Contact the Debtor. |

| MS03 | Not Specified Reason Agent Generated | • Only used in case national legislation does not allow the use of AC04, AM04, MD07, RR01, RR02, RR03, and RR04. e.g. in Germany. | Contact the Debtor. |

| RC01 | Bank Identifier Incorrect / Invalid BIC of the recipient | • Originator: the provided BIC for a non-EEA SEPA SDD collection is not complete (BIC8 instead of BIC11). | • Contact the Counterparty for the correct BIC for a non-EEA SDD collection. |

| RR01 | Missing Debtor Account Or Identification | • Missing details about the Debtor account or identification. • Note: This code cannot be used in certain SEPA countries for reasons of data protection. MS03 could be used as an alternative. | • Contact the Debtor for the correct BIC of a non-EEA SDD Collection. • Ask Creditor PSP to allocate the correct and complete BIC of the Debtor PSP in the inter-PSP message. |

| SL01 | Specific Service Offered By Debtor Agent | • All Debtor–Invoked consumer-right rejects: 1. Creditor blocking; 2. Collection amount limitations; 3. Collection frequency limitations Other services offered by the Debtor PSP. | Contact the Debtor. |

Autogiro - mapping

Autogiro reason codes are communicated to Atlar by Bankgirot, the local Swedish Clearing House. For failed Autogiro collections (Direct Debits) we will send you the reason codes to understand what happened to an underlying direct debit.

| Reason Code | Definition |

|---|---|

| CANAMENDCOMM_ | Cancelled/Changed Payments Comment Code |

| REJECTCOMM_ | Rejected Payments Comment Code |

| SPECSTATUS_ | Payments Specification Status Code |

| MANDADVINFO_ | Mandate Advice Information Code |

| MANDADVCOMM_ | Mandate Advice Comment Code |

Autogiro - Payment Specification Status Codes

| Reason Code | Meaning | Suggested Action |

|---|---|---|

| SPECSTATUS_0 | Approved payment, payment executed | No Action needed. |

| SPECSTATUS_1 | Insufficient funds, payment not executed | Contact the debtor to top-up the account or agree upon an alternative payment method. |

| SPECSTATUS_2 | No connection to Autogiro (bank account closed), or the payer's bank has not approved the withdrawal (Other reason). The payment has not been executed | Contact the debtor for updated bank account information or agree upon an alternative payment method. |

| SPECSTATUS_9 | Renewed funds, payment not executed but retry will be attempted if agreement in place. Note: Renewed funds only applies to incoming payments. | In case retries are configured and you’re still unable to collect the funds, contact the debtor to agree upon a payment method. |

Autogiro – Rejected Payments Comment Codes

| Reason Code | Meaning | Suggested Action |

|---|---|---|

| REJECTCOMM_01 | Omitted, mandate not found | Make sure that you’ve sent the mandate details to the bank using Atlar’s dashboard or API. Alternatively, you can migrate active mandates to Atlar by flagging the status active. In the latter case, Atlar will not send the mandates to Bankgirot. |

| REJECTCOMM_02 | Omitted, account not approved or closed | Contact the debtor to agree upon an alternative payment method. |

| REJECTCOMM_04 | Incorrect payer number | Make sure that the mandate ID is correct and resubmit the collection to Bankgirot. |

| REJECTCOMM_06 | Incorrect period code | Not applicable. |

| REJECTCOMM_07 | Incorrect number for recurring payments | Not applicable. |

| REJECTCOMM_08 REJECTCOMM_09 | Amount non-numeric Ban on outgoing payments | Not applicable. |

| REJECTCOMM_10 | Bankgiro number not found at Bankgirot | Not applicable. |

| REJECTCOMM_12 | Incorrect payment date | The payment date you specify may not be later than the current year plus two calendar years. Note that Atlar allows you to schedule payments for maximum of 60 days in the future. |

| REJECTCOMM_13 | Payment date passed | The payment date has passed and the debtor did not have enough funds available. Contact the debtor to top-up the account or agree upon an alternative payment method. |

| REJECTCOMM_15 | The payee bankgiro numbers in the opening record and the transaction record are not the same | Not applicable. |

| REJECTCOMM_24 | Amount exceeds Max. amount | Initiate a new collection with the appropriate amount. The upper limit has been set previously while configuring Autogiro with your bank. |

Autogiro – Cancellation/amendment of payments Comment codes

| Comment Code | Meaning | Suggested Action |

|---|---|---|

| CANAMENDCOMM_01 | Incorrect payment date | The payment date you specify may not be later than the current year plus two calendar years. |

| CANAMENDCOMM_02 | Incorrect payer number | Make sure that the mandate ID is correct. |

| CANAMENDCOMM_04 | Incorrect transaction code (occurs when 32 or 82 are missing) | Not applicable |

| CANAMENDCOMM_05 | Incorrect amount | Initiate a new collection with the appropriate amount. The upper limit has been set previously while configuring Autogiro with your bank. |

| CANAMENDCOMM_06 | Incorrect new payment date | The changed payment date is not within limits required by Autogiro. The payment date you specify may not be later than the current year plus two calendar years. |

| CANAMENDCOMM_10 | Incorrect payee bankgiro number (incorrect check digit) | Not applicable. |

| CANAMENDCOMM_11 | Payee bankgiro number missing (zero or blank) | Not applicable. |

| CANAMENDCOMM_12 | Cancelled | Contact your debtor to agree upon an alternative payment method or configure a new Autogiro mandate. |

| CANAMENDCOMM_13 | Payment missing, not processed | Not applicable. |

| CANAMENDCOMM_14 | Amended payment date | No action needed. |

| CANAMENDCOMM_15 | Note amended, recurring payment order | No action needed. |

| CANAMENDCOMM_18 | Amended payment date | No action needed. |

Autogiro - Mandate Advice Information Codes

| Information Code | Meaning | Suggested Action |

|---|---|---|

| MANDADVINFO_03 | Cancellation. Initiated by payee | Contact the debtor to agree on another means of payment. |

| MANDADVINFO_04 | New addition. Initiated by payee | No action needed. |

| MANDADVINFO_05 | Change payer number. Only permitted for mandates based on bank account number. Initiated by payee. | No action needed. |

| MANDADVINFO_10 | Cancelled due to payee’s bankgiro number being closed. Initiated by payee or payee’s bank | Not applicable. |

| MANDADVINFO_42 | Response to account inquiry from bank on new payer in Autogiro | Not applicable. |

| MANDADVINFO_43 | Cancelled/removed due to unanswered account inquiry | Not applicable. |

| MANDADVINFO_44 | Cancelled due to payer’s bankgiro number being closed. Initiated by payer’s bank | Not applicable. |

| MANDADVINFO_46 | Cancellation. Initiated by payer or payer’s bank | Contact the debtor for another means of payment or configure a new Autogiro mandate. |

Autogiro – Mandate Advice Comment Codes

| Comment Code | Meaning | Suggested Action |

|---|---|---|

| MANDADVCOMM_02 | Mandate canceled on the initiative of payer or payer’s bank | Contact the debtor for another means of payment or configure a new Autogiro mandate. |

| MANDADVCOMM_03 | Account type not approved for Autogiro | Contact the debtor for the correct account details – for example, a checking account instead of the savings account. |

| MANDADVCOMM_04 | Mandate not found in Bankgirot’s mandate directory | Make sure that the mandate has been sent to Bankgirot and activated. If not, resend the mandate details using Atlar’s API or Dashboard. |

| MANDADVCOMM_05 | Incorrect bank account or personal details | Contact the debtor for correct details. |

| MANDADVCOMM_07 | Cancelled/removed due to unanswered account inquiry | Not applicable. |

| MANDADVCOMM_09 | Payer Bankgiro number not found at Bankgirot | Not applicable. |

| MANDADVCOMM_10 | The payer number/mandateID you have specified for this mandate is already registered in Bankgirot's mandate directory.The combination of payer number/mandateID and payee Bankgiro number must be unique. Bankgirot ignores the new mandate and the existing mandate remains in use.Has been cancelled and cannot be registered until seven (7) Bank days have passed: The payer number you have specified has been used for another payer within the last seven (7) Bank days. | Mandate is already registered in Bankgirot's directory: Check the payer number and civic number that you specified. If you: - Have sent a duplicate you do not need to do anything. - Want to register a new mandate with the same civic number – change the payer number on the mandate and resend it to Bankgirot. Has been cancelled and cannot be registered until seven (7) Bank days have passed: Check the payer number and civic number that you specified. If you want to register a new mandate with the same payer number that was previously cancelled, you need to wait seven (7) Bank days before you resend the mandate. |

| MANDADVCOMM_20 | Incorrect civic/company number or agreement on mandate based on bankgiro number not found | Correct the civic/company number. Contact the debtor if necessary. |

| MANDADVCOMM_21 | Incorrect payer number | Make sure that the mandate ID is correct. |

| MANDADVCOMM_23 | Incorrect bank account number | Check the account number against the payer’s mandate form. Contact the debtor to correct the account number of the payer. |

| MANDADVCOMM_29 | Incorrect payee bankgiro number | Not applicable. |

| MANDADVCOMM_30 | Deregistered payee bankgiro number | Not applicable. |

| MANDADVCOMM_32 | New mandate | You can now send payment initiations associated with this mandate to Bankgirot. |

| MANDADVCOMM_33 | Cancelled | Not applicable. |

| MANDADVCOMM_98 | Mandate cancelled due to cancelled payer bankgiro number | Ask the payer to fill in a new mandate with a valid Bankgiro number or agree on another payment method. |

Payment schemes and Timings

Payment timings differ across schemes; this section provides you with a general overview. However, it’s important to note that there are differences between banks in how they handle timings — we cover this during your onboarding to your respective banks.

SEPA

SEPA Credit Transfer

SEPA Credit Transfers reach the recipient account within one business day. In case a payment has been sent prior to the underlying bank’s cut-off time, the payment will be settled the same day. In case the payment was sent after the cutoff it will reach the recipient within one business day.

SEPA Instant Credit Transfer

SEPA Instant Credit Transfers are processed instantly 24/7/365. In most cases, the money is available to the recipient within 10 seconds after the payment has been sent.

SEPA Direct Debit CORE

Collections can be made straight away when a mandate has been signed with the customer. For the majority of banks, the direct debit collection instruction must be sent to the bank at least one business day prior to the requested collection date.

SEPA Direct Debit B2B

Collections can be made after the debtor bank has validated the existence of the mandate. It has to be noted that the creditor will not receive a notification regarding the mandate activation status. Thus, it has to be tested by initiating a direct debit collection. For the majority of banks, the direct debit collection instruction must be sent to the bank at least one business day prior to the requested collection date.

Sweden

Swedish account transfer

Swedish account-to-account transfers reach the recipient account within one business day. In case a payment has been sent prior to the underlying bank’s cut-off time, the payment will be settled same-day. In case the payment was sent after the cutoff it will reach the recipient within one business day.

Swedish giro payment

Swedish Giro – BankGiro & PlusGiro – payments reach the recipient account within 1 business day. In case a payment has been sent prior to the underlying bank’s cut-off time, the payment will be settled the same day. In case the payment was sent after the cutoff it will reach the recipient within 1 business day.

Autogiro

New mandates can take up to 6 business days before they’re activated and collections can be made. Collection instructions must be sent to the bank at least 1 business day prior to the requested collection date.

Denmark

Danish account transfers

Standard Credit Transfers

Standard Credit Transfers will arrive the following business day if the payment was sent to the bank prior to the cut-off. In case the payment order is sent after the cut-off, the payment will reach the recipient’s account two business days after it is sent.

Same-day Credit Transfers

Same-day credit transfers reach the recipient’s account the same day if the payment order was sent to the bank prior to the cut-off. In case the payment order is sent after the cut-off, the payment will reach the recipient’s account one business day after it is sent.

Immediate Credit Transfers

Immediate credit transfers are processed instantly 24/7/365 can be used for payments up to DKK 500,000. The money is made available to the recipient within seconds after the payment order is sent by the debtor.

Betalingsservice

Mandates will be registered by next business day if sent to MasterCard prior to 5:30pm CET. Collections can be made one business day after a mandate has been registered. The deadline for submissions to Betalingsservice is 9am CET six working days before the end of the month preceding the month in which you wish to take the payment. Example: You wish to collect in September, so you need to send a payment request to Betalingsservice 6 working days before the end of August.

International

Cross-border bank transfers

Cross-border bank transfers are financial transactions where the debtor and creditor are based in separate countries or when the debtor and creditor are in the same market but transacting in a third currency. In the case of SEPA countries, a transaction would classify as cross-border if the currency transacted in is not the Euro. For example, a Swedish company with a Danish currency account initiates a payment to a company based in Denmark with a Danish bank account.

Cross-border payments are sent through the SWIFT (System for Worldwide Interbank Financial Telecommunications) messaging system and leverage the concept of correspondent banking to settle the funds. As cross-border payments are sent over SWIFT, they require an IBAN and a BIC to identify the recipient account.

The amount of time it takes for a cross-border payment usually ranges from one to five days. If the payment has been initiated prior to the cut-off time, it will be processed the same day.

Account Identifiers

Account identifiers differ across markets. This section provides you with a general overview of the five types of Account Identifiers used by Atlar.

| Account Identifier Type | Description | Additional Info |

|---|---|---|

| IBAN | International Bank Account Number | The International Bank Account Number is a unique account identifier that contains all necessary information of a bank account. The number contains a two letter country code, bank and branch information and the account number. There is no uniform length for the IBAN but the maximum length is 34 characters. |

| BBAN | Basic Bank Account Number | The Basic Bank Account Number is a country specific unique account number. Each country has their own BBAN standard but the number mostly consist of a bank identifier and account number. For country specific examples please check the table below. |

| DEPRECATED The Bank specific Account Number is an unique account number at a bank without any bank identifier (e.g. routing or clearing number). Each country and bank can have their own account number standards but the number is mostly alphanumeric. It's important to note that the Account Number identifier type requires the BIC to be provided with it. Not all payment schemes can be used with this identifier, please provide IBAN for all countries that support IBANs. | ||

| SE_BG | Swedish Bankgiro Number | The Bankgiro Number is a unique account number that consist of 7 or 8 digits and is used by the Swedish Bankgirot clearing system. |

| SE_PG | Swedish PlusGiro Number | The PlusGiro Number is also a unique account number used in Sweden by the PlusGirot clearing system. The number consists of 2 to 8 digits. |

Country specific account identifiers

Atlar performs validation on country specific account identifiers. This table provides you with more details.

| Market code | Market | Routing | BBAN | IBAN | Comment | |

|---|---|---|---|---|---|---|

| AT | Austria | 5 digits | 11 digits | 5 digit routing + 11 digit account number | 20 characters | |

| AU | Australia | 6 digits | 6-10 digits | 6 digit routing + 6-10 digit account number | - | Routing is referred to as BSB number |

| BE | Belgium | 3 digits | 9 digits | - | 16 characters | |

| BG | Bulgaria | 4 digits | 8 digits | - | 22 characters | |

| CA | Canada | 8 digits | 7-12 digits | 8 digit routing + 7-12 digits account number | - | |

| CH | Switzerland | 5 digits | 12 digits | 5 digit routing + 12 digit account number | 21 characters | |

| CN | China | 12 digits | 14-19 digits | 12 digit routing + 14-19 digit account number | - | Routing is referred to as CNAPS number |

| CZ | Czech Republic | 4 digits | 16 digits | - | 24 characters | |

| DE | Germany | 8 digits | 10 digits | 8 digit routing + 10 digit account number | 22 characters | Routing is referred to as BLZ number |

| DK | Denmark | 4 digits | 9 digits | 4 digit routing + 9 digit account number | 18 characters | |

| ES | Spain | 8 digits | 12 digits | 8 digit routing + 12 digit account number | 24 characters | |

| FI | Finland | - | - | - | 18 characters | |

| FR | France | - | 11 upper and lower case alphanumeric characters | - | 27 characters | |

| GB | United Kingdom | 6 digits | 8 digits | 6 digit routing + 8 digit account number | 22 characters | |

| GH | Ghana | - | - | - | - | |

| GR | Greece | 7 digits | 16 upper and lower case alphanumeric characters | 7 digit routing + 16 upper and lower case alphanumeric character account number | 27 characters | |

| HR | Croatia | 7 digits | 10 digit | 7 digit routing + 10 digit account number | 21 characters | |

| HU | Hungary | - | 17 digits | - | 28 characters | |

| IE | Ireland | 4 upper and lower case alphanumeric characters + 6 digits | 8 digits | 4 upper and lower case alphanumeric characters + 6 digits routing + 8 digit account number | 22 characters | |

| IT | Italy | c5n5n | 12c | c5n5n routing + 12c account number | 27 characters | |

| IN | India | 11 digits | 10-20 digits | 11 digits routing + 10-20 account number | - | |

| LT | Lithuania | - | 11 digits | - | 20 characters | |

| LU | Luxembourg | - | 13 upper and lower case alphanumeric characters | - | 20 characters | |

| MX | Mexico | - | - | 18 digit CLABE number | - | Use 18 digit CLABE number |

| NL | Netherlands | - | 10 digits | - | 18 characters | |

| NO | Norway | - | 7 digits | - | 15 characters | |

| PL | Poland | 10 digits | 16 digits | 10 digit routing + 16 digit account number | 28 characters | |

| PT | Portugal | 8 digits | 13 digits | 8 digit routing + 13 digit account number | 25 characters | |

| RO | Romania | - | 16 upper and lower case alphanumeric characters | - | 24 characters | |

| SE | Sweden | 4 digits* | 6-20 digits | 4 digit* routing + 6-20 digit account number | 24 characters | |

| SI | Slovenia | 5 digits | 10 digits | 5 digit routing + 10 digit account number | 19 characters | |

| SK | Slovakia | - | 16 digits | - | 24 characters | |

| US | United States | 9 digits | 6-17 digits | 9 digit routing + 6-17 digit account number | - | Routing is referred to as ABA number |

| VN | Vietnam | - | 1-20 digits | - | - |

Account identifiers per scheme

Cross border

For CROSS_BORDER use IBAN and BIC or BBAN and BIC.

SEPA

For SCT, SCT_INST and SDD_CORE use IBAN.

Domestic schemes

- United Kingdom: For GB_CT_FPS and GB_CT_BACS use BBAN or IBAN

- Sweden: For SE_A2A use BBAN or IBAN, for SE_GIRO use BG_NR or PG_NR and for AUTOGIRO use BBAN

- Denmark For DK_A2A, DK_A2A_SAMEDAY and DK_A2A_INST use BBAN or IBAN

- Switzerland: For CH_CT use IBAN

Updated 11 months ago