Payment Details

OverviewThis page explains how payments and mandates transition through various statuses in Atlar,

along with typical timings for different payment schemes.

Use these details as guidance, not as a strict state machine.

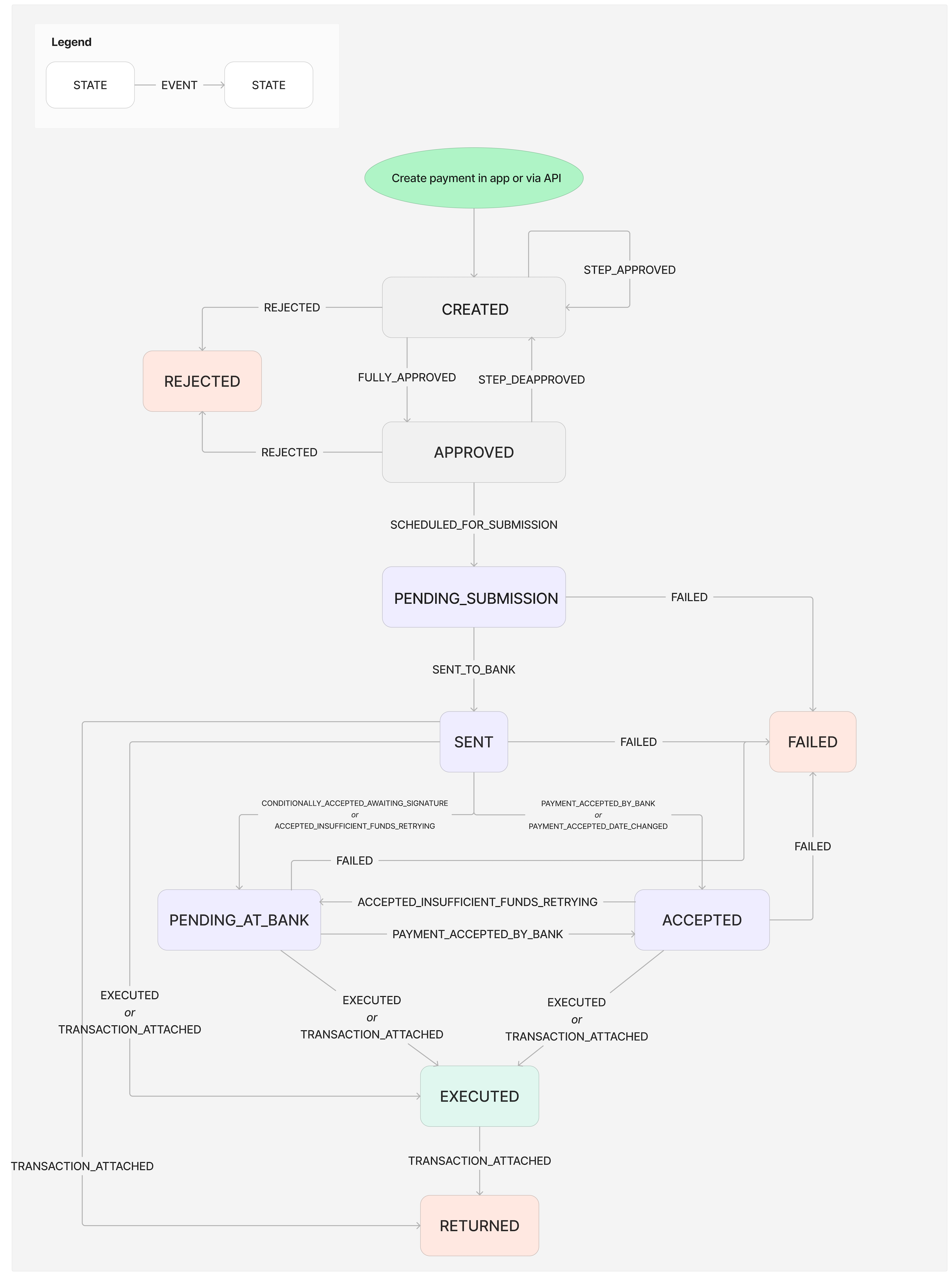

Payment statuses

Use the diagram below to understand how Payments (credit transfers and direct debits) transition through various statuses.

Important Guidance

- It is not recommended to lock client logic strictly to the diagram below.

- The state machine is for understanding, not a guarantee of what will always occur.

- Atlar may add new events (not statuses) or transitions without breaking backwards compatibility.

- In rare cases (bank or Atlar issues), an operator may force-update a payment’s status.

This generates an event:OPERATOR_FORCE_UPDATEand updates the entity to a new status.

| State | Description |

|---|---|

CREATED | Payment has been created and is pending approval. |

REJECTED | Payment has been rejected by the customer. |

APPROVED | Payment has been approved by the customer. |

PENDING_SUBMISSION | Atlar is submitting the payment to the bank. Editing is no longer possible. |

SENT | Payment has been sent to the bank. |

PENDING_AT_BANK | Payment is pending at the bank (e.g., insufficient funds, or awaiting bank-side signature). |

ACCEPTED | Payment has been received and accepted by the bank. |

EXECUTED | Payment has been executed by the bank. |

FAILED | Payment has failed. |

RECONCILED | Payment has been reconciled to a transaction on your account statement. |

RETURNED | Payment has been returned by the bank. |

UNKNOWN | Payment’s status is unknown. |

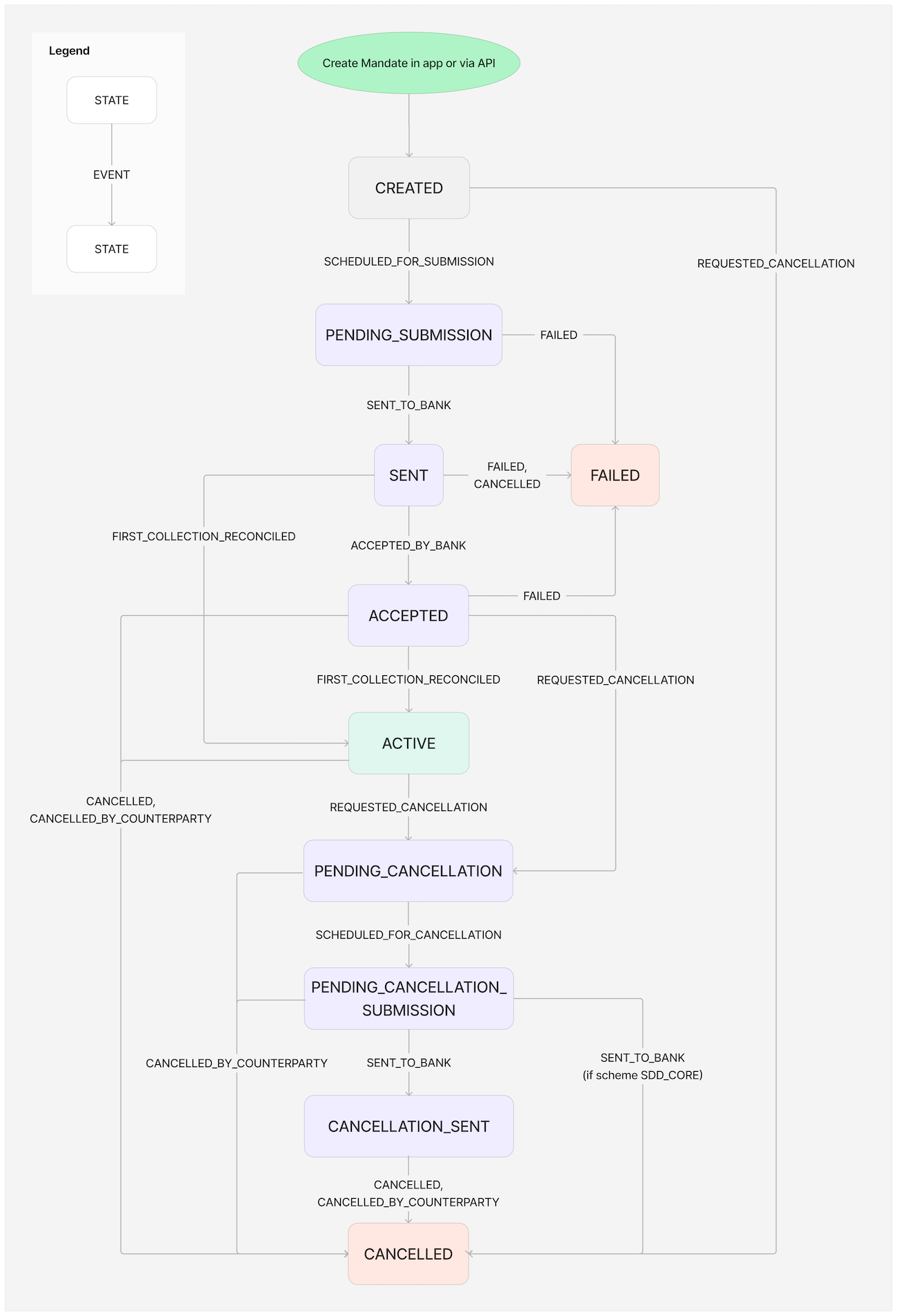

(Direct-Debit) Mandate statuses

The diagram below shows how Mandates transition through various statuses.

While Atlar treats changes to possible transitions as a non-breaking API change,

it is not recommended to lock client logic strictly to the diagram.

| State | Description |

|---|---|

CREATED | Mandate is created (active=false). How the mandate is sent to the bank depends on the scheme (e.g., Autogiro mandates are sent directly, SDD mandates are sent with the first payment). |

PENDING_SUBMISSION | Atlar is submitting the mandate to the bank. The mandate can no longer be edited. |

SENT | Mandate has been sent to the bank. |

ACCEPTED | Mandate has been received and accepted by the bank. |

ACTIVE | Mandate is active, either after the first reconciled collection or if created with active=true. |

PENDING_CANCELLATION | A cancellation request has been issued. Atlar will submit the cancellation shortly. |

PENDING_CANCELLATION_SUBMISSION | Atlar is submitting the cancellation to the bank. |

CANCELLATION_SENT | Cancellation of the mandate has been sent to the bank. |

FAILED | Mandate failed to register (bank or Atlar error). |

CANCELLED | Mandate has been cancelled by you or the counterparty. |

UNKNOWN | Mandate’s status is unknown. |

Payment schemes and timings

Payment timings differ across schemes and banks.

The information below provides a general overview—your onboarding with Atlar will cover bank-specific cut-off times and nuances.

SEPA

SEPA Credit Transfer

- Funds typically reach the recipient within one business day.

- If sent before the bank’s cut-off, settlement occurs the same day.

- If sent after the cut-off, settlement occurs next business day.

SEPA Instant Credit Transfer

- Processed instantly (24/7/365).

- Funds are usually available within 10 seconds of initiation.

SEPA Direct Debit CORE

- Collections can begin immediately after a mandate is signed.

- Most banks require the collection instruction to be submitted at least one business day before the collection date.

SEPA Direct Debit B2B

- Collections can begin after the debtor bank validates the mandate.

- The creditor does not receive confirmation of activation;

validation is confirmed by attempting a collection. - Most banks require instructions one business day before the collection date.

Sweden

Swedish account transfer

- Reaches the recipient within one business day.

- Same-day settlement if sent before the bank’s cut-off.

Swedish giro payment (BankGiro & PlusGiro)

- Reaches the recipient within one business day.

- Same-day settlement if sent before the bank’s cut-off.

Autogiro

- New mandates may take up to 6 business days to activate.

- Collection instructions must be submitted at least one business day before the collection date.

Denmark

Standard Credit Transfers

- Arrive the next business day if sent before cut-off.

- If sent after cut-off, arrive in two business days.

Same-day Credit Transfers

- Same-day arrival if sent before cut-off.

- If sent after cut-off, arrival is next business day.

Immediate Credit Transfers

- Processed instantly 24/7/365, for payments up to DKK 500,000.

Betalingsservice

- Mandates are registered by the next business day if sent to MasterCard before 5:30pm CET.

- Collections can be made one business day after registration.

- Submissions must be sent 9am CET six working days before the end of the prior month

(e.g., to collect in September, send by six working days before the end of August).

International

Cross-border bank transfers

- Cross-border payments involve parties in different countries or in the same country using a third currency.

- SEPA transactions are considered cross-border if the currency is not EUR.

- Sent over SWIFT using IBAN and BIC for settlement.

- Typical processing time: 1–5 days, depending on cut-off and correspondent banks.

- If initiated before the bank’s cut-off, processing usually begins same day.

Account Identifiers

Account identifiers differ across markets.

This section provides a general overview of the four types of account identifiers used by Atlar.

| Account Identifier Type | Description | Additional Info |

|---|---|---|

| IBAN | International Bank Account Number | The International Bank Account Number (IBAN) is a unique account identifier that contains all necessary information of a bank account. The number contains a two-letter country code, bank and branch information, and the account number. There is no uniform length for the IBAN, but the maximum length is 34 characters. Not all countries use IBANs. |

| NUMBER | Bank specific account number | The bank-specific Account Number is a unique account number at a bank without any bank identifier (e.g., routing or clearing number). Each country and bank can have their own account number standards, but the number is mostly numeric and in some cases alphanumeric. Different countries have different rules for this type of identifier. For example, a British (GB) NUMBER should be 8 digits (domestically referred to as the account number), whereas a Swedish (SE) NUMBER should be 8 to 17 digits, including both the clearing number and the account number. To specify a British sort code, use a Routing Identifier. The SWIFT code (BIC) is also considered a Routing Identifier. If the country supports IBANs, an IBAN identifier is superior to NUMBER in terms of payment scheme availability and payment success rate. |

| SE_BANKGIRO | Swedish Bankgiro Number | The Bankgiro Number is a unique account number that consists of 7 or 8 digits and is used by the Swedish Bankgirot clearing system. |

| SE_PLUSGIRO | Swedish PlusGiro Number | The PlusGiro Number is also a unique account number used in Sweden by the PlusGirot clearing system. The number consists of 2 to 8 digits. |

Country specific account identifiers

Atlar performs validation on country-specific account identifiers.

This table provides more details.

| Market code | Market | IBAN | NUMBER | Routing | Comment |

|---|---|---|---|---|---|

| AT | Austria | 20 characters | 11 digit account number | 5 digits (AT_DLZ) | Use IBAN |

| AU | Australia | – | 6-10 digit account number | 6 digits (AU_BSB) | |

| BE | Belgium | 16 characters | – | – | |

| BG | Bulgaria | 22 characters | – | – | |

| CA | Canada | – | 7-12 digit account number | 9 digits (CA_CPA) | Routing consists of transit number and financial institution number. If given as 8 (5+3) digits, prepend 0. |

| CH | Switzerland | 21 characters | – | – | Use IBAN |

| CN | China | – | 14-19 digit account number | 12 digits (CN_APS) | |

| CZ | Czech Republic | 24 characters | – | – | |

| DE | Germany | 22 characters | 10 digit account number | 8 digits | Use IBAN |

| DK | Denmark | 18 characters | 13 digit account number | – | |

| ES | Spain | 24 characters | 12 digit account number | 8 digits | Use IBAN |

| FI | Finland | 18 characters | – | – | |

| FR | France | 27 characters | – | – | |

| GB | United Kingdom | 22 characters | 8 digit account number | 6 digits (GB_DSC) | GB_DSC is most often referred to as Sort Code |

| GH | Ghana | – | – | – | |

| GR | Greece | 27 characters | 16-character alphanumeric account number | 7 digits | Use IBAN |

| HR | Croatia | 21 characters | 10 digit account number | 7 digits | |

| HU | Hungary | 28 characters | – | – | |

| IE | Ireland | 22 characters | 8 digit account number | 6 digits | Use IBAN |

| IT | Italy | 27 characters | c5n5n routing + 12c account number | c5n5n | Use IBAN |

| IN | India | – | 10-20 digit account number | 11 digits | |

| LT | Lithuania | 20 characters | – | – | |

| LU | Luxembourg | 20 characters | – | – | |

| NL | Netherlands | 18 characters | – | – | |

| NO | Norway | 15 characters | – | – | |

| PL | Poland | 28 characters | 16 digit account number | 8 digits (PL_KNR) | |

| PT | Portugal | 25 characters | 13 digit account number | 8 digits | Use IBAN |

| RO | Romania | 24 characters | – | – | |

| SE | Sweden | 24 characters | 4-5 digit clearing number + 4-12 digit account number | – | e.g. ccccaaaaaaa where c is a clearing digit and a is an account number digit |

| SI | Slovenia | 19 characters | 10 digit account number | 5 digits | |

| SK | Slovakia | 24 characters | – | – | |

| US | United States | – | 6-17 digit account number | 9 digits (US_ABA) | |

| VN | Vietnam | – | – | – |

Updated 10 months ago